The global television market is undergoing significant structural change. While overall TV shipments have seen modest declines in recent years, certain manufacturers are gaining momentum, while others are rethinking their entire business models to remain competitive.

Two developments stand out in particular: the rapid rise of TCL Technology and a major strategic shift by Sony Group Corporation.

TCL Grows Despite Market Slowdown

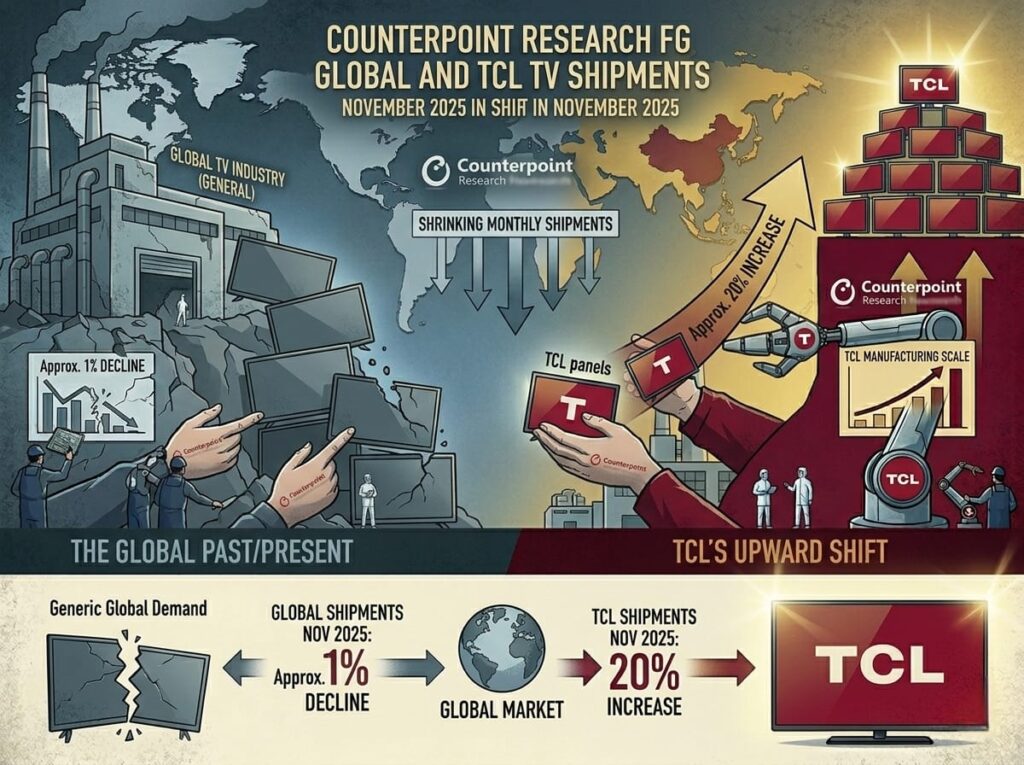

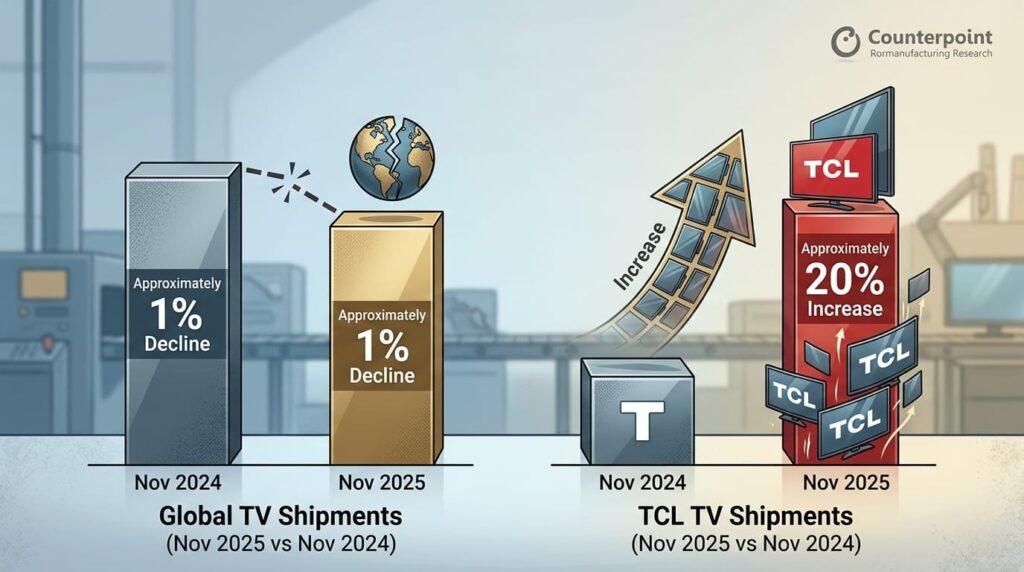

According to recent data from Counterpoint Research, global TV shipments declined by approximately 1 percent year over year in November 2025. Yet during the same period, TCL increased its TV shipments by around 20 percent compared to the previous year.

This is not a short term anomaly. It reflects a broader strategy that has been unfolding for several years.

TCL has focused aggressively on:

- Competitive pricing

- Large screen formats of 75 inches and above

- Mini LED backlighting technology

- Integration of Google TV

Importantly, this growth does not mean TCL has fully taken over the premium segment. However, it clearly positions the company as a much stronger global contender than it was just a few years ago.

Growth Comes at Someone’s Expense

Market share shifts rarely happen in isolation.

Recent shipment trends show Samsung Electronics declining slightly from 18 percent to 17 percent global share, while TCL narrowed the gap significantly, rising from 13 percent to approximately 16 percent.

Hisense reportedly fell from 12 percent to 10 percent, while LG Electronics increased modestly from 8 percent to 9 percent.

Samsung continues to lead globally across entry level to premium categories. However, as Samsung pushes further into high end OLED and Neo QLED positioning, a window has opened in the upper midrange segment. TCL has entered that space aggressively, especially in large screen Mini LED models where consumer demand remains strong.

A key differentiator has also been software. While Samsung relies on its proprietary Tizen platform, TCL’s adoption of Google TV offers a widely familiar interface, broad app availability, and tight integration with the Google ecosystem, which many consumers perceive as an advantage.

The Bigger Picture: A Saturated, Highly Competitive Market

The TV market today is mature. Growth is no longer driven by first time buyers, but by upgrades and size expansion.

Within this landscape:

- Samsung remains the overall volume leader

- LG continues to dominate the OLED panel segment and invests in advanced display innovation

- Sony has maintained strong brand value in the premium segment

But Sony is now at a strategic crossroads.

Sony’s Strategic Pivot: Partnership Instead of Full Control

Sony recently announced plans to form a strategic joint venture with TCL that would manage its home entertainment division, including the Sony BRAVIA television lineup.

Under the proposed structure, TCL would hold 51 percent of the new entity, while Sony would retain 49 percent. The binding agreement is expected to be finalized by March 2026, with operational activity projected to begin in 2027.

If completed, 2026 could mark the final year in which Sony independently develops, manufactures, and distributes televisions on its own.

This is not a full acquisition. It represents a shift in operating model.

TCL would take responsibility for manufacturing, logistics, and operational scale. Sony would maintain control over its core strengths, including picture processing, video engineering, motion algorithms, and proprietary chipsets that differentiate BRAVIA models.

Learning from History

The Japanese TV industry has already seen dramatic consolidation over the past two decades. Once dominant brands such as Toshiba, Hitachi, Mitsubishi, JVC, and even Panasonic have either exited the TV business or significantly reduced their presence.

Rising production costs, aggressive competition from South Korean leaders like Samsung and LG, and later from Chinese manufacturers, eroded margins across the sector.

Sony survived largely by repositioning itself firmly in the premium space. By avoiding the low cost segment and emphasizing picture processing excellence, color accuracy, and cinematic positioning, it preserved brand equity.

However, even a premium strategy is not immune to structural market pressure. Development costs remain high, margins are tight, and Sony increasingly prioritizes growth areas such as gaming, content, music, and film production.

The partnership model reduces operational burden while preserving engineering influence.

What Does TCL Gain?

For TCL, the partnership presents both opportunity and scrutiny.

Benefits include:

- Deeper access to the premium market

- Association with a globally respected brand

- Exposure to Sony’s advanced image processing expertise

Challenges include:

- Heightened quality expectations

- Increased global visibility

- Responsibility for protecting Sony’s brand identity

In an optimistic scenario, the combination could be powerful:

- Sony contributes decades of image science and motion processing expertise

- TCL contributes massive manufacturing scale and supply chain efficiency

The result could be premium televisions at more competitive price points, and continued performance improvements in TCL’s own branded models.

Not a Story of Winners and Losers

The 2026 television market story is less about one company rising while another falls, and more about structural transformation.

We are seeing:

- A shift from full vertical control to strategic partnerships

- A redistribution of manufacturing power toward China

- Increasing importance of cost efficiency and supply chain control

- Narrowing technological gaps between brands

TCL is growing rapidly, but it still faces intense competition. Sony is evolving, not disappearing.

And consumers may ultimately benefit the most. If partnerships successfully combine engineering excellence with production efficiency, the outcome could be better performance at more accessible prices.

The global TV race is no longer simply about who sells the most units. It is about who adapts fastest to a changing competitive landscape.